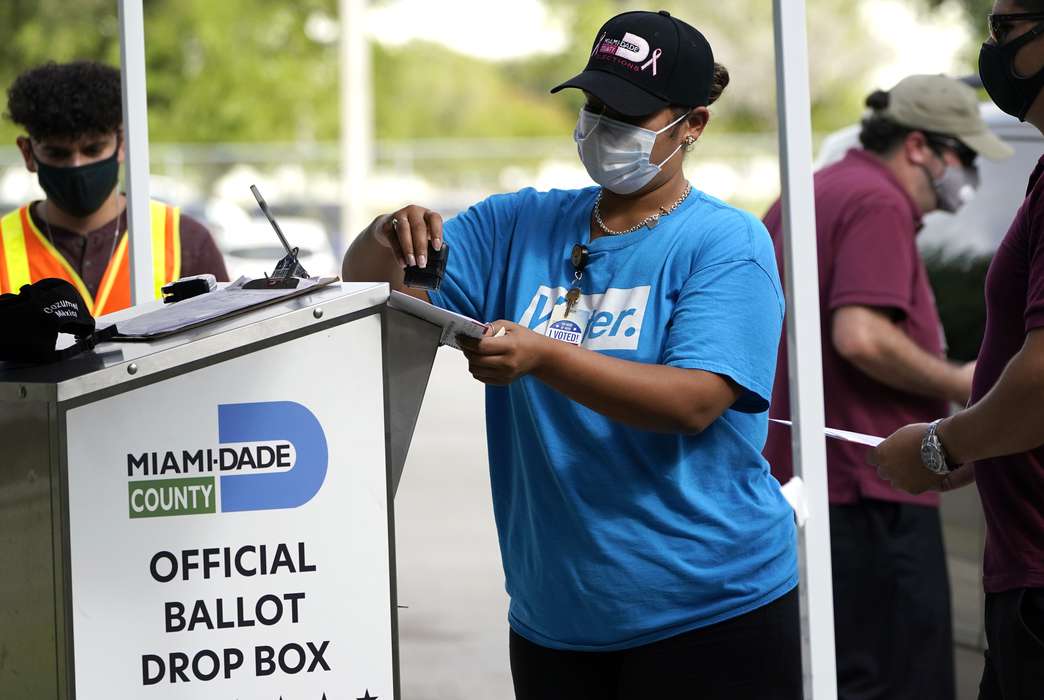

Local banks improve community resilience during recessions

Small banks and credit unions are better for neighborhoods. (AP Photo/Julie Jacobson)

Areas of the U.S. with more branches of large Wall Street banks experienced higher unemployment and slower recovery from the Great Recession than regions with more localized financial institutions, according to a new study that researchers say has serious implications for the current economic crisis.

Specifically, counties with a concentration of community bank and credit union branches one standard deviation higher than normal experienced a drop in employment due to the recession that was up to 0.84% less than average each year from 2007 through 2010, researchers from Reed College found in a new paper for the Socio-Economic Review.

By contrast, counties with a concentration of big bank branches one standard deviation higher than average saw increases in the unemployment rate that were between 0.11% and 0.25% higher.

The researchers said their findings, which were controlled for factors such as housing market conditions and racial demographics, show that local banking systems can increase communities’ resilience during recessions. They also said their results counteract arguments by some economists that localized financial institutions are more fragile than big banks.

“Small and local organizations seem to tie the local economies much more to employment than in cases where economies are populated by large-scale or for-profit, market-based banks,” said lead author Marc Schneiberg, a sociologist at Reed, which is located in Portland, Oregon. “Having a substantial segment of local small-scale stakeholder capitalism seems to be a platform for a more general shared prosperity.”

The Great Recession was driven largely by excessively risky financial instruments like mortgage-backed securities being utilized by Wall Street bankers. Big banks that were exposed to risk had to dramatically curtail lending, hurting local economies across the U.S.

The coronavirus pandemic, on the other hand, is not a crisis created by the financial system, and banks have performed far better so far during the current crisis than in 2008. More support is available to smaller firms because of policies like the Paycheck Protection Program, while booming equity markets have given larger firms an easy source of fundraising. But despite the big banks’ resilience this time around, Schneiberg said that his findings still have serious implications for the ongoing economic recovery.

“Big banks may have a more productive role to play in this recovery than the other, but you’re still going to have the question of what do banks do when their clients are in trouble,” said Schneiberg, who wrote the paper alongside former Reed student Eleanor Parmentier.

For example, a community bank that has a longstanding relationship with a local bar that has been shuttered for months because of COVID-19 restrictions may be more lenient about repayment of a loan than a big bank like Citigroup or Wells Fargo. That’s because community banks have a larger incentive to keep their region’s economy afloat than multinational banks, whose operations are not limited to a single region and can rake in billions from non-lending activities like equities trading. They’re also more attuned to the idiosyncrasies of specific small businesses and less reliant on impersonal metrics like FICO scores.

This difference will likely give areas with stronger community banks and credit unions a leg up in 2021 and beyond, according to Schneiberg.

"There’s still value in being deeply embedded in a local economy, to know and feel its rhythms,” he said.

The researchers used two statistical models in their work: a cross-period strategy to assess relationships between pre-crisis banking structure and unemployment by year, and a time series analysis of panel data to test the moderating effects of different banking structure types on broader unemployment.

Using the number of bank and credit union branches as a measure of institutions’ footprints in a given county was an imperfect technique, Schneiberg said, and as online banking proliferates during the pandemic, a similar study of banking in the 2020s may not be able to use the same metric.

“We ended up settling on branches because a lot of banking, even with fintech, is still face-to-face, and a lot of business lending is still face-to-face, especially in the early 2000s,” he said.

Schneiberg believes that lawmakers should take more steps to help community banks and credit unions.

“Make sure we continue to support and cultivate local and small-scale forms of banking when you do broad reforms,” he said.

But Schneiberg still sees a role for large banks in the U.S. economy, as long as the financial system is diversified.

“You want to have big banks that can draw on global and national sources of capital,” he said. “I don’t think large scale banking is under any threat in this country.”

The paper, titled “Banking structure, economic resilience and unemployment trajectories in US counties during the great recession,” is forthcoming in the Socio-Economic Review. The co-authors are Marc Schneiberg and Eleanor Parmentier of Reed College.

Related sections

Social Sciences

Repeal of Florida felon ban didn't increase voter turnout in most-impacted communities

Engineering, Physical Sciences

Just one sensor can create 3D images of rooms via echolocation

Engineering, Life Sciences

Surgical tools are sometimes left inside patients. This X-ray archive can help mitigate the damage.

Business & Economics

Overseas employees might help US employers save money on taxes

Life Sciences

Recent transfer of malaria parasites to monkeys may lead to more outbreaks

By Miles Martin

Mind & Behavior, Social Sciences

Home health aides, other welfare support workers could face elevated risk of suicide

Physical Sciences

The ocean on Saturn’s moon Enceladus might not be very old

Physical Sciences, Life Sciences, Business & Economics

Expected dampening of wildfires could be weakened by deforestation

Life Sciences, Social Sciences

More US students are vaping weed, but the increases vary by racial group

Engineering, Life Sciences, Physical Sciences

Human tissues can be grown on this new sandwich-like scaffold

By Tara DiMaio